Scott Kahan on Investing: Trump Boom or Gloom and Doom?

Scott Kahan: Trump Boom or Gloom and Doom? It wasn’t long ago that stock futures signaled a dramatic market decline in response to the electoral victory of Donald Trump as POTUS 45. Since then the market’s been pretty much straight up. Go figure? Certified Financial Planner and President of Financial Asset Management Corp. in Chappaqua and NYC, Scott Kahan talks about how to keep your emotions in check when investing in the age of Trump-onomics!

How do you explain the Trump rally?

After the election the market expected a sell off but we had a major rally.

After the election the market expected a sell off but we had a major rally.

The reason is that uncertainty was eliminated in the market. No one knows what would have happened with a Hillary win. Maybe we would have had a Hillary rally. Because the economy has been doing well.

When you add in the prospect of lower taxes, regulatory reform and increased infrastructure spending that’s a good environment for business. And that changed the market’s outlook.

Emotions are running high?

We talk a lot about taking the emotions out of investing and that goes for politics as well. People have to winnow out their political emotions and look at economic reality.

Many people are aghast at the prospects of a Trump presidency and see gloom and doom. Others are euphoric and see the shackles being taken off the business community and expect an economic boom. Don’t be overly optimistic but don’t be too pessimistic.

The economic trends have been good and we have a new pro-growth president. The Dow just hit 20,000. That’s cause for optimism. On the other hand there still is uncertainty about what Trump is really going to do – we all know he is prone to contradictory statements – and how he is going to get it done.

The economic trends have been good and we have a new pro-growth president. The Dow just hit 20,000. That’s cause for optimism. On the other hand there still is uncertainty about what Trump is really going to do – we all know he is prone to contradictory statements – and how he is going to get it done.

He has appointed a conservative cabinet and has a Republican Congress but on things like infrastructure spending – that’s a traditionally Democratic initiative that Republicans have opposed. Will they do an about face? Or will he be able to put together a coalition of moderate Republicans and Democrats to get this done?

If he wins on infrastructure and delivers on tax cuts that could be a formula for exploding the debt. So whatever your political preferences there’s reason for optimism and there’s also ample uncertainty. That’s a reason to curb your enthusiasm.

What inning are we in?

That’s the issue. Are we in the eighth inning of a growing economy or are we at the start of something new. You can make predictions based on Trump’s policies but nobody is really sure what they are. I think we’re somewhere in the middle with pent up growth for the next year or so.

That’s the issue. Are we in the eighth inning of a growing economy or are we at the start of something new. You can make predictions based on Trump’s policies but nobody is really sure what they are. I think we’re somewhere in the middle with pent up growth for the next year or so.

What sectors are the potential winners and losers under Trumponomics?

In this rally small caps and banks are doing well. Energy stocks should do well with regulatory reform. But if the economy continues to grow we should see across the board growth for all companies. If Trump gets his infrastructure spending, companies like Caterpillar and Deere do well.

What about health care?

Tough to predict because nobody knows what’s going to happen? Will the ACA be repealed? What kinds of fixes will be put in its place? This sector is fraught with uncertainty. If they can get a handle on drug prices that can’t be good for health companies so that’s a sector to be wary of now.

Small caps vs. large caps?

We believe in being diversified and small caps usually outperform large caps over time. I think small caps will continue to do well but I wouldn’t overweight. You just have to be diversified in large and small caps, and that includes emerging markets.

The Fed is signaling up to 3 rate increases in 2017.

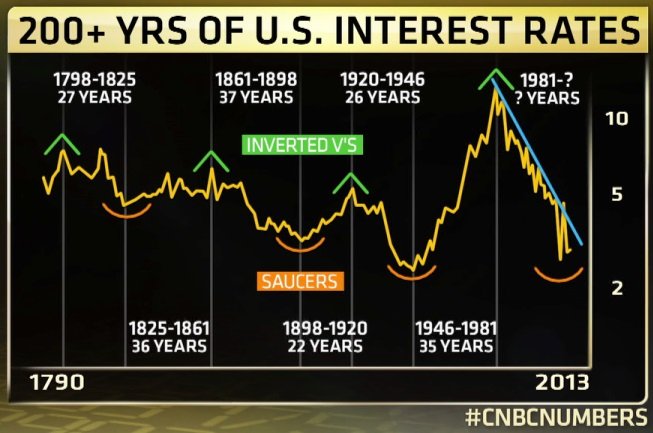

Louise Yamadas Historical Interest Rates

Nobody knows how many rate increases there will be. What’s important to understand is that we are in the beginning of a long-term cycle of rising interest rates. But rates don’t go straight up. They tend to move in 30-year cycles. Look back to the 1970s, CD rates were 15%, mortgage rates 12-15%. Rates didn’t bottom out until recently. These are predictable long-term trends.

Is there good news about rising rates?

The good news about higher rates is that income investors will be rewarded. And it usually means the economy is doing well because the Fed won’t act if the economy softens. But there’s an emotional hurdle to investing in fixed income securities in a rising rate environment.

Don’t chase yield and stay on the shorter end of fixed income. Build your bond ladders, whether it’s with individual bonds, funds or ETFs, so you have money coming due every year to lock in at higher rates. You don’t want to have to sell fixed income at a loss to cover expenses – because bond prices drop when rates rise. As part of a diversified portfolio you should also have an emergency fund set aside to cover at least 3 months of expenses.

Don’t chase yield and stay on the shorter end of fixed income. Build your bond ladders, whether it’s with individual bonds, funds or ETFs, so you have money coming due every year to lock in at higher rates. You don’t want to have to sell fixed income at a loss to cover expenses – because bond prices drop when rates rise. As part of a diversified portfolio you should also have an emergency fund set aside to cover at least 3 months of expenses.

What about high yield bonds?

High yields have bounced back 16% in the last year. In a growing economy they should continue to do well, even with rising rates. We recommend 3-8% of your portfolio in high yields or a combination of high yields and preferred stocks. Don’t try to pick bonds. Buy a fund or ETF that is diversified with maturities and domestic and foreign bonds. And stay on the short side.

Before you look into a high yield asset, or any asset that you’re looking at for diversification, look inside the funds you currently own. You may already have exposure to high yield or foreign assets in your current portfolio.

It all comes down to planning…

Planning helps take the emotions out of investing. When will you need your money? When will you need income from your investments?

Plan your portfolio, cash and securities, with these factors in mind. Look at total return, capital appreciation plus interest and dividends. Set your asset allocations against your time horizon needs and rebalance when your allocations deviate from your plan.

Taking the emotions out of investing

We review client’s portfolios monthly but you don’t have to rebalance unless your allocations move out of the ranges you’ve set.

Rebalancing forces you to sell high and buy low. This is difficult for investors because when stocks surge and bond prices drop its hard to sell “winners” to buy depressed assets. But if your plan is a 50/50 stock/bond portfolio and a stocks rally leaves you at 60/40 – you have to rebalance to 50/50. That’s how you take the emotions out of investing.

Financial Asset Management Corporation has provided fee-only financial planning and wealth management services for individuals and small businesses in the Tri-State area since 1986. They serve 150 clients and manage over 200 million dollars in assets. FAM Corp. President Scott Kahan is a Certified Financial Planner professional. (Financial Asset Management Corp., 26 South Greeley Avenue, Chappaqua, NY, (914) 238-8900; www.famcorporation.com)

More like this

You may also like

Editor's Choice

Bucket List