Scott Kahan: Taking the emotions out of investing

Chappaqua resident Scott M. Kahan, Certified Financial Planner professional and President of New York City based Financial Asset Management Corp., recently opened a branch of his fee-only wealth management practice in Chappaqua. We sat down with him to discuss the importance of financial planning. Here’s what he had to say.

What does a Certified Financial Planner do?

Anyone can call themselves a financial planner. A Certified Financial Planner professional (CFP ®) should follow a fiduciary standard that puts the clients interests first. We establish goals and objectives so we know what the client is trying to accomplish. I use an example that if you want to go on a trip you don’t just get in your car and start driving. You first discuss where you want to go, how to get there, what stops you want to make, make sure you have extra money if your car breaks down. Financial planning is the map and the investments, tax returns, estate planning documents, etc. are the part of the vehicles to get you where you want to go.

The key is to establish a client’s financial goals. In other words, what is your time horizon? When will you need your money and what you will need it for. Two clients may be looking for income and capital preservation. One is saving for a home. The other already owns a home. Those are two very different portfolios. Are you retired or saving for retirement or your children’s college education? Will you need the money in 5, 10 or 15 years? Each scenario requires it’s own portfolio.

The key is to establish a client’s financial goals. In other words, what is your time horizon? When will you need your money and what you will need it for. Two clients may be looking for income and capital preservation. One is saving for a home. The other already owns a home. Those are two very different portfolios. Are you retired or saving for retirement or your children’s college education? Will you need the money in 5, 10 or 15 years? Each scenario requires it’s own portfolio.

We try to take the emotions out of investing for clients. That means finding out what a client’s relationship is with money and how much risk do they want to take or need to take. This is often referred to as risk tolerance. We have a questionnaire to help us establish an investor’s risk tolerance but that’s a starting point. You have to probe between the lines. It’s sort of like being a financial therapist at times.

Aren’t risk tolerance and time horizon inextricably tied?

Tactically speaking, yes. But an investor’s emotions are his or her emotions independent of time horizon. We know that for most investors their relationship with money goes back to childhood and how money was treated then. This is important to know. If you ask a person with  a million dollars what percentage of their portfolio they would be comfortable losing in a downturn they might say 20%. But ask them if they would be comfortable seeing their portfolio dip by $200,000 and they might say, “No, that’s too much.” That client’s risk tolerance is not 20% no matter what their time horizon may be. That said, looking at time horizon can help an investor better understand their real risk tolerance. Planners should help people understand their relationship with money or risk tolerance and tie it back to their goals and objectives or time horizon.

a million dollars what percentage of their portfolio they would be comfortable losing in a downturn they might say 20%. But ask them if they would be comfortable seeing their portfolio dip by $200,000 and they might say, “No, that’s too much.” That client’s risk tolerance is not 20% no matter what their time horizon may be. That said, looking at time horizon can help an investor better understand their real risk tolerance. Planners should help people understand their relationship with money or risk tolerance and tie it back to their goals and objectives or time horizon.

How do you manage a client’s emotions?

First is establishing a cash portion of a portfolio. Retirees should have 1 to 2 years of cash set aside so they don’t have to sell securities to raise cash for living expenses. Second is rebalancing your portfolio. Once we have determined a client’s financial goals and structured a portfolio for them, say 50% equities and 50% fixed income; we monitor their accounts monthly and rebalance quarterly to maintain their portfolio structure. If the stock market goes up, your portfolio may rise to 60% equity. That’s when you sell equities, buy fixed income and rebalance at 50/50.

So you don’t say, “I’m feeling lucky. Let it ride!”

Right. Rebalancing is the key to taking the emotions out of investing. And there’s nothing like buying low and selling high to keep your emotions in check. That’s the goal.

What kinds of questions are investors asking you?

Most people are concerned about the markets, the economy and everything from Ebola to ISIS. Sometimes they have too much of a product orientation. There’s a glut of information available to investors from television, the internet and people pushing products. Most of my clients need more than investment advice. Their portfolios may be well invested but they’re not sure what to do next because the portfolio doesn’t reflect where they are going. They need financial planning, a road map of how to accomplish their goals. From there we can determine how to structure a portfolio for the long term.

How do you invest for income/capital preservation in a rising interest rate environment?

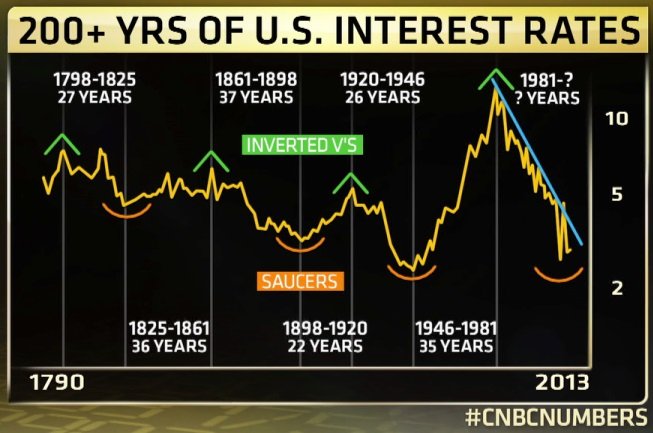

Louise Yamadas chart of 222 years of interest-rates

Look for shorter time horizons and ETFs – 1 to 3 or 4 years on bonds. For the last 3 years everyone expected rates to rise. They didn’t. Now we’re looking at 2015 or 2016 for the first Fed rate hike. Investors, understandably, have been willing to sacrifice yield for protection. But historically interest rate cycles take 30 years to play out. They don’t go up over night. Remember when CDs were yielding 18% and mortgage rates were 12%. It took a long time for interest rates to unwind. If you ladder your fixed income purchases with short-term maturities you can manage through rising cycles. And even clients who want capital preservation should be in stocks to combat inflation and maintain purchasing power. We focus on total return – looking at bonds and equities together.

Do you like dividend stocks and high yield bonds to boost yield?

We believe there is a place in a portfolio for high yield short-term bonds. Same with dividend stocks, but don’t rely on them for the bulk of your portfolio because there is risk involved. Investors often mistake dividend stocks as a substitute for bonds. You have to remember that they are equities. When the market goes down 20% your stock may follow. People say, “Well I won’t sell them.” Are you sure? What did you do in 2008-9?

Some people say dividend stocks will get hammered when rates rise. Others say rising interest rates mean the economy is doing well and so will stocks.

Too often investors buy dividend-paying stocks without understanding the downside risk.Overall, if the market rises for 2 years, which it can, if you own a dividend paying stock you should be fine because they act like an equity first and foremost and you will get capital appreciation along with the dividend.. But when the market goes down, dividend-paying stocks will fall as well. You continue to receive the dividend, but your value will be lower. Dividend stocks are fine as long as you don’t sell when the market goes down and understand that they have risk. They’re not bonds.

What about ETFs?

What about ETFs?

An ETF is an exchange-traded fund structured as indexes, like the S&P index or a bond index. They have tax advantages because unlike a mutual fund that distributes profits, with an ETF you control when you sell and thus when you receive distributions. They also have low fees compared to mutual funds. However, they are often thinly traded. So you have to make sure you know what you are buying. There are also trading strategy ETFs that use hedging strategies to boost return. We try to avoid them and stick with widely traded index ETFs.

How about defined maturity ETFs?

We use some iShares – especially with fixed incomes. Their defined maturities help you ladder a bond portfolio. They fluctuate in value so they are not trading vehicles. But if you hold them to maturity you get your principal back just like a bond. It’s another way to take the emotions out of investing?

What’s your take on preferred stocks?

Okay for diversification. Say 5% of a portfolio. But they are essentially long-term bonds. There’s not as much volatility as an equity but the income will be there. On the other hand when interest rates rise they are somewhat protected because their yields are so high. (Closed end funds with preferred stocks?)

Annuities? TIPS?

Not a big fan of annuities. It’s not a good time to buy a fixed annuity – better to buy when rates are high. A variable annuity offers tax deferral but there are high fees and expenses that reduce your returns. They are often sold with the idea of safety but the person selling them usually is earning a commission. When you pull money out you’re paying a tax bill then. TIPS should be part of an income strategy, especially if you anticipate inflation but right now we’re not seeing much inflation.

What advice do you have for people investing for college?

We do a seminar every year at Greeley High School and if there is one take away from those sessions it is don’t set up an UTMA (Uniform Transfers to Minors Act) custodial account for your child. The tax advantages from shifting investment income to your child are minimal and they work against your child if you are applying for financial aid. Worse yet, at 21 the money is legally the child’s and they can do what they want with it. Like buying a sports car. Or worse. We recommend 529 plans and for New Yorkers definitely stick with the NY State program for the tax deduction. Go to nysaves.org for more information.

We do a seminar every year at Greeley High School and if there is one take away from those sessions it is don’t set up an UTMA (Uniform Transfers to Minors Act) custodial account for your child. The tax advantages from shifting investment income to your child are minimal and they work against your child if you are applying for financial aid. Worse yet, at 21 the money is legally the child’s and they can do what they want with it. Like buying a sports car. Or worse. We recommend 529 plans and for New Yorkers definitely stick with the NY State program for the tax deduction. Go to nysaves.org for more information.

Have you ever seen a more difficult investing environment?

Yes. In 2008-9 we were very close to a depression. Technology adds to some of the issues. Life is easier but there is too much information that people don’t know what to do with. TV talking heads who predicted the last crash may have also predicted many crashes that didn’t happen. The economy is looking better. Markets always get better. Why shouldn’t they again?

Financial Asset Management Corporation has provided fee-only financial planning and wealth management services for individuals and small businesses in the Tri-State area since 1986. They serve 140 clients and manage over 150 million dollars in assets. FAM Corp. President Scott Kahan is a Certified Financial Planner professional and has served on the Board of Directors for the Horace Greeley Scholarship Fund. (Financial Asset Management Corp., 26 South Greeley Avenue, Chappaqua, NY, (914) 238-8900; www.famcorporation.com)

More like this

You may also like

Editor's Choice

Bucket List