Kahan on Inflation: Part 3

Kahan on Inflation: Part 3

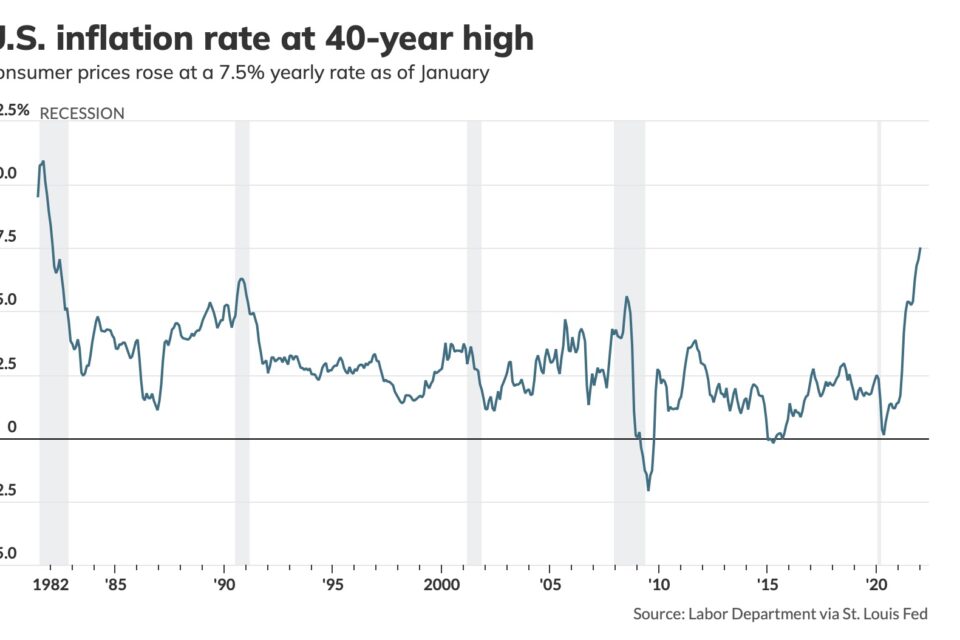

For the third time in the past eight months we are checking in with Scott Kahan on inflation. Last June the Certified Financial Planner professional and President of Financial Asset Management Corp. in Chappaqua and NYC, talked about the comparisons investment gurus were making between today’s economy and the Roaring Twenties. Two post pandemic periods that saw a rising stock market. We followed that discussion last October as inflation numbers reached five percent for the first time. Today new CPI numbers were released for January that saw inflation hit 7.5% – a forty year high.

What do you make of today’s CPI numbers for January?

What do you make of today’s CPI numbers for January?

Obviously, the inflation in our economy has persisted longer than Federal Reserve Bank Chairman Powell had hoped and has arguably reached heights he never anticipated. And what is equally obvious is that inflation will be, once again in 2022, the dominant theme in any discussion of the US economy and its financial markets.

That said, while the level inflation has reached should not be trivialized, it is important to note that what turns inflation into entrenched inflation is wage inflation – something that we are seeing to a certain extent but not an alarming level. Which is why we continue to view inflation as something that will return to the two, two and a half percent range economists have been predicting.

Why has it jumped so high?

First, it is important to remember that inflation typically is a sign of a robust economy and in our current frame of reference this is certainly true. The US economy grew at 5.7% in 2021 – the highest rate since 1984. And unemployment has dropped from a pandemic high of 14.7% in April 2020 to 4% today. The economy is strong. People are working and spending money. A strong economy naturally feeds inflation.

Both the strength of the economy and the inflation level we see are related to the pandemic and the supply chain issues associated with it. And the nature of the pandemic which has curtailed certain aspects of our service economy, such as travel and entertainment. And funneled money into tangible goods purchases which puts even more stress on the supply chain. The strength of the economy coupled with funneling of consumer spending into tangible goods buckets is why we saw the CPI number we saw today.

How are your client’s reacting to current economic and market issues?

I would have to say that my client’s are susceptible to the same forces that are, almost inexplicably, causing Americans in survey after survey to express their economic pessimism. I say inexplicable because it is hard to reconcile such a strong economy with such pessimism. Which I think gets back to COVID. People are tired of COVID. Burned out on COVID. And it leads to pessimism.

How has this pessimism manifested itself?

A few weeks ago, when the market was selling off some of our clients were concerned that we were in for a major correction. This is it. The big one. They felt they had too much money in equities and it was time to get out. It’s very difficult for people to believe the market could be so strong when everybody feels so bad. Which is why we have to remind ourselves that economic growth is strong and unemployment is low.

So how did you deal with that?

We reminded our client’s that we don’t make investment decisions based on market timing but on how closely our portfolios reflect the market allocations we have developed to both help them reach their financial goals and respect their risk profile. In some cases, we had client’s whose portfolio had a significant run up beyond their preferred 60/40 ratio. Some reaching as high as 70%. So we trimmed their equity positions and reallocated the money into short and intermediate term fixed income. No more than ten years.

We reminded our client’s that we don’t make investment decisions based on market timing but on how closely our portfolios reflect the market allocations we have developed to both help them reach their financial goals and respect their risk profile. In some cases, we had client’s whose portfolio had a significant run up beyond their preferred 60/40 ratio. Some reaching as high as 70%. So we trimmed their equity positions and reallocated the money into short and intermediate term fixed income. No more than ten years.

In other cases, we had clients whose portfolios have been chronically under weight equities despite their stated plans and risk tolerance and we let them run. That’s how a good financial plan and a disciplined approach to portfolio balancing helps take the emotions out of investing and helps investors avoid trying to time the market. Look at March 2020 the market crashed, and it looked like it would be years to come back but it came back in months – record time. If you pulled out then it becomes hard to get back in. You can’t time the market!

Next stop the Fed…

Yes, so inflation inevitably leads to interest rate hikes – that’s the tool the Fed uses to control inflation. And everybody knows it’s coming but we don’t know when or how much. Insiders believe we will see the first Fed hike in March. And we will see a series of hikes throughout the year. The hopes and expectations are that a Fed rate of two to two and a half percent, coupled with changing consumer habits as people begin to travel again and return to the office will ease supply chain issues and ease inflation.

What are you telling retirees and people approaching retirement?

In the meantime, we are counseling our client’s and certainly retirees to keep their fixed income investments short term. If all goes well they may have an opportunity over the next two years or so to lock in higher rates and have a soft landing. We build a laddered bond portfolio in short and intermediate terms bonds for them. And because we believe the economy is strong we have small portions of their portfolio in short or intermediate term high yield bond funds. And most importantly, we tell our retirees to hold 12 to 18 months of expenses in cash so they are not forced to sell asset positions when they are down.

Final Words?

Yes, remember that corrections are natural and always either just in the rear view mirror or seemingly visible on the horizon. But corrections are good for the market. They make markets more efficient. If you always have sufficient cash on hand, time is on your side in the stock market.

Yes, remember that corrections are natural and always either just in the rear view mirror or seemingly visible on the horizon. But corrections are good for the market. They make markets more efficient. If you always have sufficient cash on hand, time is on your side in the stock market.

Finally, shut out the daily investment headlines and stick to your allocations. And if you are looking at your portfolio on a day-by-day basis make sure you are not just looking at the numbers from the most recent quarter. Make sure you are looking at 12 months numbers. And three, five and ten years as well. Almost invariably the longer term numbers will make you more confident to stick to your program.

Financial Asset Management Corporation has provided fee-only financial planning and investment management services for individuals and small businesses in the Tri-State area since 1986. They serve 175 clients and manage over 325 million dollars in assets. (26 South Greeley Avenue, Chappaqua, NY, (914) 238-8900; www.famcorporation.com )

More on What To Do from Scott Kahan here:

More like this

You may also like

Editor's Choice

Bucket List