Kahan on Inflation: The Elephant in the Room

Kahan on Inflation: The Elephant in the Room

Just fourteen weeks ago we checked in with Scott Kahan, a Certified Financial Planner professional and President of Financial Asset Management Corp. in Chappaqua and NYC. He gave us his take on the rising chatter about inflation and what it means for your financial plan. (See Kahan on the Roaring Twenties) As the inflationary prognosis has changed from “temporary” to “more persistent”, we thought we would check in again to see what he’s thinking.

In terms of conventional wisdom on inflation what’s changed and where are we now?

We are now at inflation levels at or exceeding five percent. What was once described as temporary are now seen as “more persistent”. Which is currently defined as months to a year. But inflation projections by most economists and market analyzers for 2024-25 are 2% – right where the Fed wants us to be.

We are now at inflation levels at or exceeding five percent. What was once described as temporary are now seen as “more persistent”. Which is currently defined as months to a year. But inflation projections by most economists and market analyzers for 2024-25 are 2% – right where the Fed wants us to be.

How do you explain this?

I think it is important to realize that most of the inflationary pressures from supply chain issues that are increasing retail prices to home prices and unmistakable signs of wage inflation are all pandemic related. And, as we are reminded daily, the pandemic is not over. And they are all arguably connected. As consumer dollars are diverted from, let’s call them pandemic sensitive parts of our economy such as travel and entertainment, to less-sensitive parts of the economy like a wide range of household items, demand for those items exceeds supply and prices go up.

Employers in turn can’t meet demand because they can’t find workers who have the skills they require. This in part is pandemic related as some workers may be less motivated to find jobs in the riskier environment of the coronavirus. Employers must increase wages to attract workers and wage inflation is now showing up in our economy.

Wage inflation being the elephant in the room

Three months ago we discussed that wage inflation was not evident. Now it is. That doesn’t mean that it will inevitably continue to rise. First, wage growth is currently showing up at the bottom end of the wage scale – I have not seen any evidence that is affecting corporate professional workers. Secondly, the bottom end of the wage scale has been stagnant for decades so we may be just playing catch up. In fact, all aspects of, however we describe our current inflationary environment, must be viewed in terms of the past decade. A period that saw inflation rates consistently below two percent. So, while the .7 and .8 percent inflation we saw in 2014 and 2015 may be over – there’s a lot of room between that and the Fed’s preferred 2%.

Three months ago we discussed that wage inflation was not evident. Now it is. That doesn’t mean that it will inevitably continue to rise. First, wage growth is currently showing up at the bottom end of the wage scale – I have not seen any evidence that is affecting corporate professional workers. Secondly, the bottom end of the wage scale has been stagnant for decades so we may be just playing catch up. In fact, all aspects of, however we describe our current inflationary environment, must be viewed in terms of the past decade. A period that saw inflation rates consistently below two percent. So, while the .7 and .8 percent inflation we saw in 2014 and 2015 may be over – there’s a lot of room between that and the Fed’s preferred 2%.

What can you tell people who are losing trust in the prognosticators?

That’s a good question because we have seen Powell and others walk back early assurances that inflation is only temporary. Two things, one is that the end of the pandemic keeps getting walked back, too. If in fact, the pandemic is a core driver of our current environment as I believe, then naturally as the pandemic timeline changes then economic forecasts are going to change.

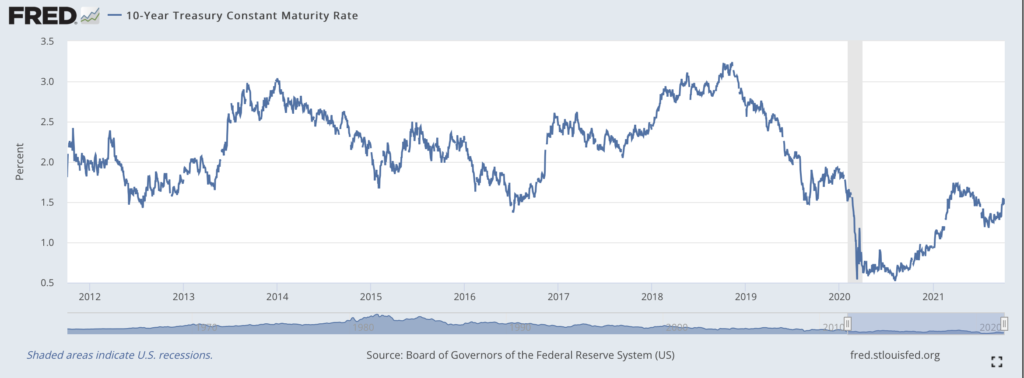

But there’s another place to look and that’s the bond market. Despite last week’s spike from 1.3 to just over 1.5% which drove stock prices down, the bond market has not over-reacted to the high inflation showing up in recent economic numbers. And we’re still at the lowest pre-pandemic levels the economy has seen in the past decade. Is the bond market telling us that inflation is not a long-term concern? Or has it not caught up to reality. Historically the bond market is accurate.

How is the combination of low interest rates and high inflation effecting your client’s retirement planning?

The value of our client’s bond portfolios has not really gone down. While our clients are counseled to stay short in maturities, we also stress diversification there. So, the return on bond funds they are invested in range from a slight drop to up 4.8%. The question I get, more often, is why I shouldn’t allocate more into equities if my bond returns are so low.

The value of our client’s bond portfolios has not really gone down. While our clients are counseled to stay short in maturities, we also stress diversification there. So, the return on bond funds they are invested in range from a slight drop to up 4.8%. The question I get, more often, is why I shouldn’t allocate more into equities if my bond returns are so low.

It’s hard to avoid that question

It is. Because on paper you are always better off, over the long term, in equities over bonds. In almost every time frame equities outperform. But we don’t advocate our clients straying from the portfolios allocations that fit their financial needs and their risk tolerance – even at times like this. And that’s because there is an emotional element in investing. If emotionally you cannot withstand more risk than a 60/40 or 50/50 portfolio than we try to stick with it because people’s biases tend toward more risk when stocks are rising and less when they are falling.

And investing is based on not having to sell assets when prices are down

That’s right. We have a 20-item questionnaire we give our clients to determine their risk tolerance. That helps determine the portfolio allocations we set – and then we stick with it – adjusting as the market dictates. Being mindful of total return, which is our core focus, helps maintain allocation discipline. Because, while our clients have perhaps 40% of their portfolio earning just 2% – their equity portfolios are up 17% to 18% over the past 12 months. So, they are, with their equity portfolios protecting against purchasing power risk associated with remaining in cash or low interest fixed income assets. And at the same time, their bond portfolios are protecting them from dumping stocks when prices are low when their fears and emotions cloud their investment decisions. Essentially, we are protecting our portfolios from ourselves.

Financial Asset Management Corporation has provided fee-only financial planning and investment management services for individuals and small businesses in the Tri-State area since 1986. They serve 175 clients and manage over 325 million dollars in assets. (26 South Greeley Avenue, Chappaqua, NY, (914) 238-8900; www.famcorporation.com )

More on What To Do from Scott Kahan here:

More like this

You may also like

Editor's Choice

Bucket List