Scott Kahan on the Market: Election Edition

Scott Kahan on the Market: Election Edition: We checked in with our “resident” financial adviser Scott Kahan, a Certified Financial Planner professional and CEO of Financial Asset Management Corp. in Chappaqua and NYC about how the election might impact the markets. “In terms of voting. Ignore the markets. And in terms of investing. Ignore the election,” he told us.

How do you explain the fastest crash and rebound in market history?

It’s pretty easy to explain the downside. You have a pandemic in a market that was already overdue for correction and you’re going to get a panic. It was the fastest 30% drop for the S&P in history. Just 22 days. It’s a sobering thought to remember that the 1929 crash took 31 days. On it’s way to a 38% bottom it racked up the four largest single-day losses in the history of the Dow. Epic.

The rebound is harder to explain. We were not expecting to see a return to market highs anytime soon. Which we have seen in the NASDAQ and the S&P – though we are still waiting for the DOW to get there. The S&P was in and out of bear market territory in just fifteen days – another record. And on August 18 it exceeded its all time high from February 19. Everything about the 2020 stock market has been historic.

How did this happen?

The biggest factor is the Fed who provided liquidity to the market and continues to demonstrate that it will be a backstop to the economy. Remember that the market is a leading indicator and it is always forecasting six months ahead. And most people think, as do I, that the worst is behind us. Businesses are reopening and we’ve learned some important lessons in terms of mitigating the virus. We know that if we have a resurgence of infections and you shut down for two weeks – the infection rates drop. So we have confidence that we can control things and that buoyed the market.

What’s the lesson of all this?

The lesson, as always, is don’t panic. Don’t try to time markets. We’ve had so many ZOOM client meetings since the pandemic started. Part of financial planning is to see people’s faces to see their reactions. The expressions of concern and surprise that they have. It helps in terms of trying to walk them off the ledge.

How do you take the emotions out of investing in this one?

The fear factor was the worst I’ve ever seen because in addition to the fear of losing your money, people were afraid of dying. I definitely had people who just wanted to sell. But when do you know when it’s time to get back in. “When I feel better.” But after we look at their situation, their financial goals of retiring, paying for college or buying a house they discover that they’re still on track. That helps them take the emotions out of investing.

Lessons learned – new questions arise?

Lessons learned – new questions arise?

The big question is what has happened to the historic dynamic between growth and value investing. Historically value outperforms growth. Especially after a big bull run of growth stocks. So coming out of a crash we would expect money to rotate into value and small cap stocks and they would lead the rebound. Instead, we see the same technology driven growth stocks leading the way out of the crash that we saw lead us up to it.

For obvious reasons. The lockdown left us stranded at home and we had to rely on technology to shop, communicate and socialize like never before – sidelining transportation, leisure and real estate. The growth narrative in tech stocks now vs. the late 90’s is so different because tech is now intertwined in every aspect of our lives and the market from health care to retail. Will we ever return to the growth value dynamics of the past?

How has this changed your client’s perspectives on their own risk tolerance?

I don’t think client’s perception of their own risk tolerances have changed much because the sell off and rebound was so fast. There was no time to reflect. As we adjust to the new normal they are not as concerned about their portfolios because it happened so quickly. Some of my clients saw the sell off as a buying opportunity. But they are a small minority. Another small minority were headstrong on selling. The great majority, however, saw it as something they have seen before and something they just had to ride out.

What advice would you give investors looking forward over the next three months – the next year?

What advice would you give investors looking forward over the next three months – the next year?

If you bought stocks when the market was down you may be overweight equities now and it’s time to take profits. That’s the ideal situation. For those who decided to wait things out, not a lot has changed. As the market returned to its previous highs their portfolios largely returned to their original allocations and they move on.

More importantly I would tell your readers that you shouldn’t be looking at the next three months or the next year. You should always view market opportunities in terms of your true time horizons. And that may be ten or twenty years if your are investing for retirement. Maybe five or ten if you are investing to pay for college or buy a house. If you have a three month or one year time horizon for any assets, that money should never be in the market. It should be in cash.

Let’s talk about the election – what happens in the market with a Biden win?

I’m not concerned about who gets elected for the economy in the short term. If Biden wins there will be more spending that will stimulate the economy even if taxes are raised. Tax rates have to go up at some point because we’re building up deficits. And we may finally see action on infrastructure. So talk about the market not liking a Biden victory are overblown. If Biden wins and Dems take over the Senate – the northeast will get their real estate tax deductions back. Concerns about Trump is about what he’s doing to this country. Climate Change will continue to be ignored. Divisiveness.

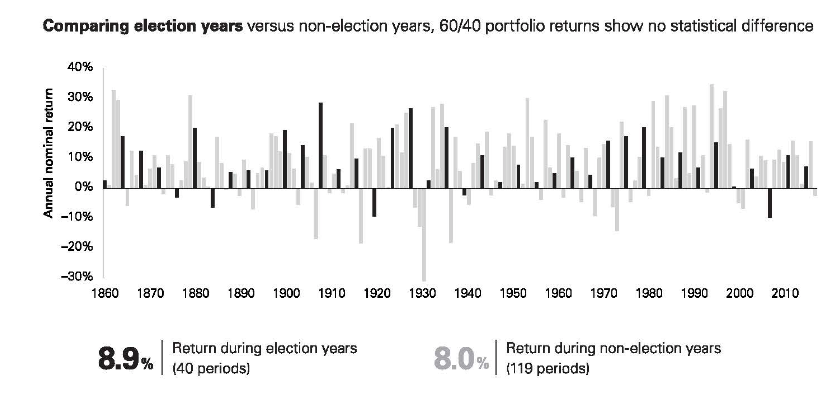

Historically, there’s not much difference in market performance between a Democrat or a Republican in office. %8.4 gains under Democrats. And 8.2% under Republicans. And election years are not more volatile than other years. On average gains during election years are 8.9% – 8% in other years. So in terms of voting. Ignore the markets. And in terms of investing. Ignore the election.

Source: Vanguard

Financial Asset Management Corporation has provided fee-only financial planning and wealth management services for individuals and small businesses in the Tri-State area since 1986. They serve 175 clients and manage over 250 million dollars in assets. (26 South Greeley Avenue, Chappaqua, NY, (914) 238-8900; www.famcorporation.com )

More on What To Do from Scott Kahan here:

More like this

You may also like

Editor's Choice

Bucket List